基于逐笔委托和逐笔成交数据构造高频因子¶

量化投资策略设计与分析的第一次作业是基于逐笔数据构造 39 个高频因子。我对高频因子的构造经验比较少,完成这个作业后的一些经验:

- 高频因子的数据格式是比较标准化的,但也要注意细节:例如空缺时间的填补等。

- 构造因子的过程本质上是数据处理的过程,常用的方法有:

groupby、resample、to_datetime、reindex、rolling、apply等。如果是非常大的数据集,应当用numpy等更快速的科学计算包,或者用C++。

39 个因子表达式¶

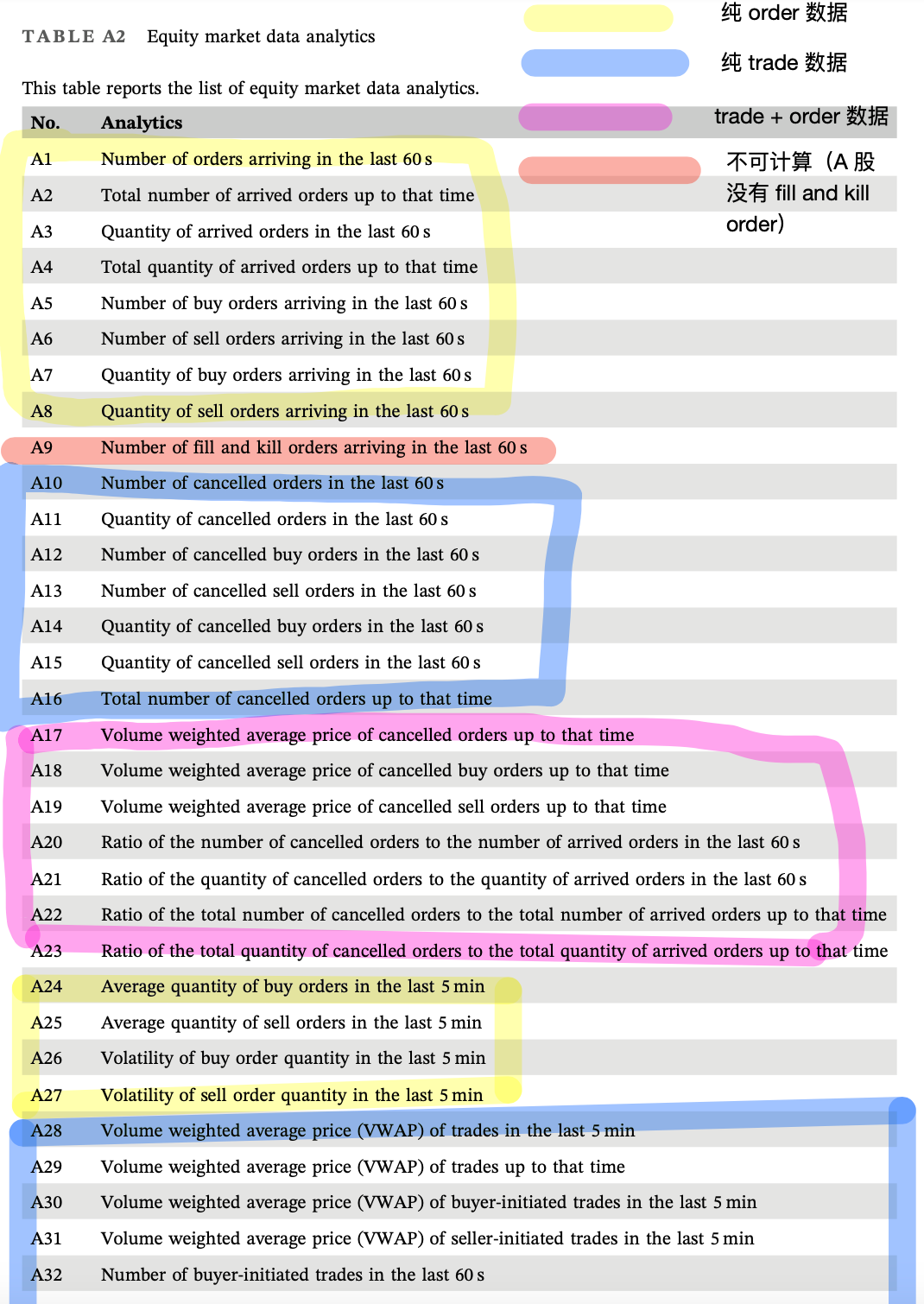

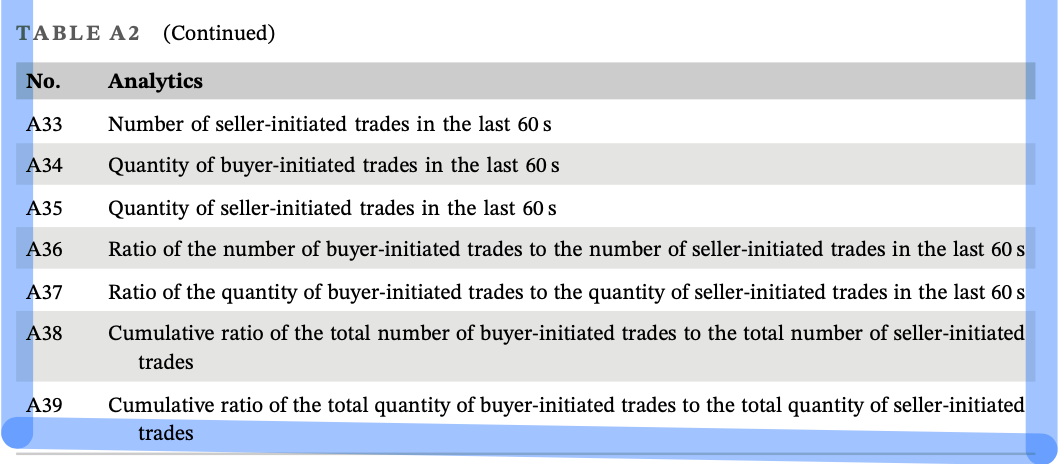

用提供的某支证券为期不超过一周的高频数据复制 Table A2 中 39 种指标。

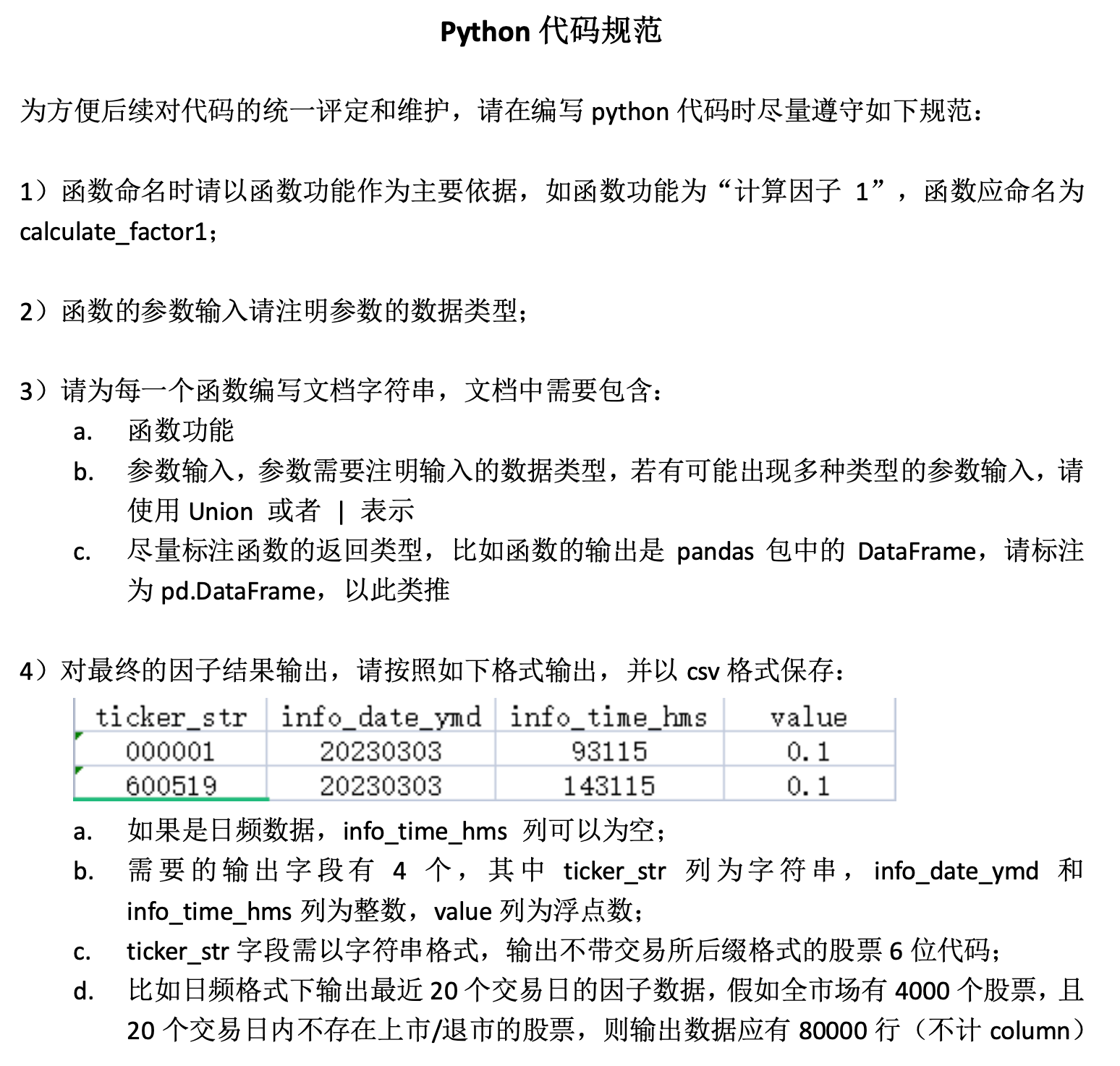

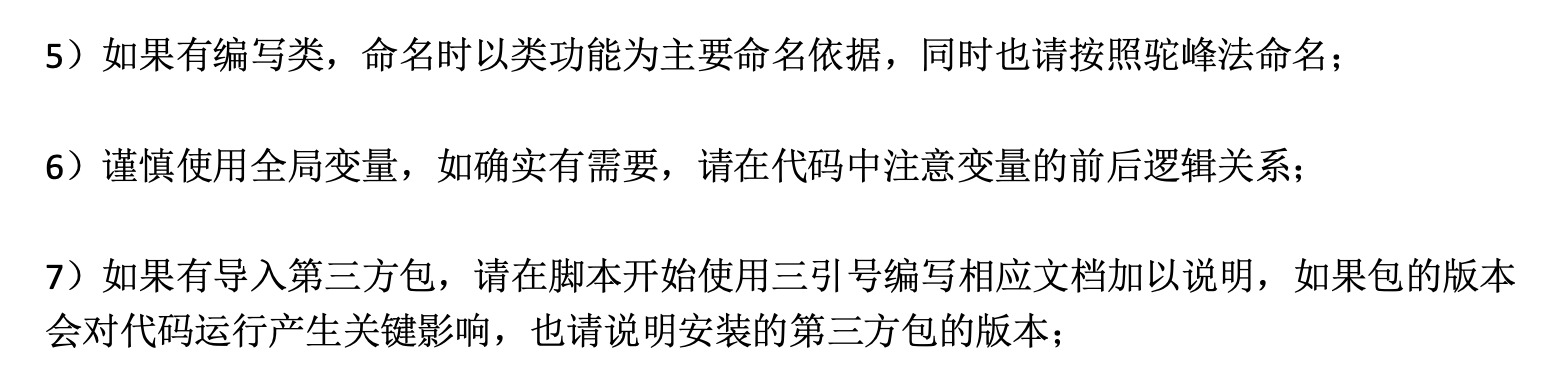

代码规范要求¶

因子计算结果¶

每天的数据范围:9:30-11:30 和 13:00-15:00,采样时点均为左开右闭,即:

- 上午从 9:31 开始有第一笔数据,11:30 为上午的最后一笔数据。

- 下午从 13:01 开始有第一笔数据,15:00 为下午的最后一笔数据。

- 每天有 240 分钟,一共 5 天,因此一共 1200 行数据。

计算因子的代码¶

自动更新类和函数中的代码更新,便于调试

导入类和函数

创建因子生成器的实例 factor_calculator

Python

factor_calculator = FactorCalculator(

order_path="./data/order_stkhf202101_000001sz.csv",

trade_path="./data/trade_stkhf202101_000001sz.csv",

factors_index_second_path="./factors/factors_index_second.csv",

)

计算所有因子,并分别导出为 csv 文件

Python

# 初始化所有因子

factors_second = None

# 逐个计算因子,并保存到本地文件,同时将所有因子合并到 factors_second 这个 DataFrame 中

for i in tqdm(range(1, 39 + 1)):

Ai = eval("factor_calculator.calculate_A" + str(i))()

# 保存单个因子到本地文件

Ai.to_csv("./factors/A" + str(i) + ".csv", index=False)

# 将单个因子添加到所有因子中

if factors_second is None:

factors_second = Ai

else:

factors_second["A" + str(i)] = Ai["A" + str(i)]

Text Only

100%|██████████| 39/39 [00:12<00:00, 3.05it/s]

将所有秒钟频率的因子导出为一个 csv 文件

Python

# 将所有因子的 index 转换为 datetime 类型

factors_second.index = pd.to_datetime(

factors_second["info_date_ymd"].astype(str)

+ " "

+ factors_second["info_time_hms"].astype(str),

format="%Y%m%d %H%M%S",

)

# 保留 9:30-11:30, 13:00-15:00 的数据,即删除 9:15-9:25 的数据

idx1 = factors_second.index.indexer_between_time("9:30", "11:30")

idx2 = factors_second.index.indexer_between_time("13:00", "15:00")

factors_second = factors_second.iloc[np.union1d(idx1, idx2)]

# 重置索引

factors_second = factors_second.reset_index(drop=True)

# 将所有因子保存到本地文件

factors_second.to_csv("./factors/all_factors_second.csv", index=False)

将秒钟频率的因子重采样为分钟频率的因子

Python

# 将秒钟频率的因子数据的 index 转换为 datetime 类型

factors_second.index = pd.to_datetime(

factors_second["info_date_ymd"].astype(str)

+ " "

+ factors_second["info_time_hms"].astype(str),

format="%Y%m%d %H%M%S",

)

# 将秒钟频率的因子数据转换为分钟频率的因子数据

factors_minute = factors_second.resample("1Min", label="right", closed="right").last()

# 保留 9:31-11:30, 13:01-15:00 的数据

idx1 = factors_minute.index.indexer_between_time("9:31", "11:30")

idx2 = factors_minute.index.indexer_between_time("13:01", "15:00")

factors_minute = factors_minute.iloc[np.union1d(idx1, idx2)]

# 导出分钟频率的因子数据

factors_minute.to_csv("./factors/all_factors_minute.csv", index=False)

构造因子的函数¶

由于代码太长,这里只放了前 5 个因子的函数,完整代码见 GitHub。

Python

"""

Author: Chao Feng

Date: 2023-03-14

Description: Functions for calculating high frequency factors

Requirements:

pandas

numpy

os

tqdm

"""

import pandas as pd

import numpy as np

import os

from tqdm import tqdm

class FactorCalculator:

def __init__(

self,

order_path: str,

trade_path: str,

factors_index_second_path: str,

) -> None:

"""

Parameters

----------

order_path : str

Path of order data

trade_path : str

Path of trade data

factors_index_second_path : str

Path of factors index with second frequency

"""

self.order_path = order_path

self.trade_path = trade_path

self.factors_index_second_path = factors_index_second_path

# 读取 order 数据

self.order = pd.read_csv(

self.order_path,

dtype={

"Exchflg": "int",

"Code": "string",

"Code_Mkt": "string",

"Qdate": "string",

"Qtime": "string",

"SetNo": "int",

"OrderRecNo": "int",

"OrderPr": "float",

"OrderVol": "float",

"OrderKind": "string",

"FunctionCode": "string",

},

)

# 读取 trade 数据

self.trade = pd.read_csv(

"./data/trade_stkhf202101_000001sz.csv",

dtype={

"Exchflg": "int",

"Code": "string",

"Code_Mkt": "string",

"Qdate": "string",

"Qtime": "string",

"SetNo": "int",

"RecNo": "int",

"BuyOrderRecNo": "int",

"SellOrderRecNo": "int",

"Tprice": "float",

"Tvolume": "float",

"Tsum": "float",

"Tvolume_accu": "float",

"OrderKind": "string",

"FunctionCode": "string",

"Trdirec": "string",

},

)

# 如果存在所有因子的数据文件,则读取因子数据

if os.path.exists(self.factors_index_second_path):

self.factors_index_second = pd.read_csv(self.factors_index_second_path)

self.factors_index_second = self.factors_index_second.set_index(

["Code_Mkt", "Qdate", "Qtime"]

)

else:

raise FileNotFoundError("Please provide the path of factors index.")

def format_factor(self, data: pd.DataFrame) -> pd.DataFrame:

"""

Format columns

Parameters

----------

data : pd.DataFrame

Data

Returns

-------

pd.DataFrame

Data with formatted columns

"""

# Reset index

data = data.reset_index()

# Rename columns

data.rename(

columns={

"Code_Mkt": "ticker_str",

"Qdate": "info_date_ymd",

"Qtime": "info_time_hms",

},

inplace=True,

)

# Change data type

data["ticker_str"] = data["ticker_str"].apply(lambda x: x.split(".")[0])

data["info_date_ymd"] = data["info_date_ymd"].apply(

lambda x: int(x.replace("-", ""))

)

data["info_time_hms"] = data["info_time_hms"].apply(

lambda x: int(x.replace(":", ""))

)

return data

def calculate_A1(self, data: pd.DataFrame = None) -> pd.DataFrame:

"""

Number of orders arriving in the last 60 s

Parameters

----------

data : pd.DataFrame

Order data

Returns

-------

pd.DataFrame

Number of orders arriving in the last 60 s

"""

# 默认使用 self.order,如果指定了 data,则使用 data 中的数据

if data is None:

data = self.order

# 按照股票、日期和秒钟分组。在组内,计算每秒的 order 数量

factor = data.groupby(["Code_Mkt", "Qdate", "Qtime"])["OrderRecNo"].count()

# 对比 factor_index,填补缺失值为 0

factor = factor.reindex(self.factors_index_second.index, fill_value=0)

# 按照股票和日期分组。在组内,对于每一秒,计算过去 60 秒的 order 数量之和

factor = (

factor.groupby(by=["Code_Mkt", "Qdate"])

.rolling(60, closed="left")

.sum()

.droplevel(level=[0, 1])

)

# 整理格式

factor = self.format_factor(factor)

factor.rename(

columns={

"OrderRecNo": "A1",

},

inplace=True,

)

factor["A1"] = factor["A1"].astype(float)

return factor

def calculate_A2(self, data: pd.DataFrame = None) -> pd.DataFrame:

"""

Total number of arrived orders up to that time

Parameters

----------

data : pd.DataFrame

Order data

Returns

-------

pd.DataFrame

Total number of arrived orders up to that time

"""

# 默认使用 self.order,如果指定了 data,则使用 data 中的数据

if data is None:

data = self.order

# 按照股票、日期和秒钟分组。在组内,计算每秒的 order 数量

factor = data.groupby(["Code_Mkt", "Qdate", "Qtime"])["OrderRecNo"].count()

# 对比 factor_index,填补缺失值为 0

factor = factor.reindex(self.factors_index_second.index, fill_value=0)

# 按照股票和日期分组。在组内,对于每一秒,计算当前累积的 order 数量之和

factor = factor.groupby(by=["Code_Mkt", "Qdate"]).cumsum().shift(1)

# 整理格式

factor = self.format_factor(factor)

factor.rename(

columns={

"OrderRecNo": "A2",

},

inplace=True,

)

factor["A2"] = factor["A2"].astype(float)

return factor

def calculate_A3(self, data: pd.DataFrame = None) -> pd.DataFrame:

"""

Quantity of arrived orders in the last 60 s

Parameters

----------

data : pd.DataFrame

Order data

Returns

-------

pd.DataFrame

Quantity of arrived orders in the last 60 s

"""

# 默认使用 self.order,如果指定了 data,则使用 data 中的数据

if data is None:

data = self.order

# 按照股票、日期和秒钟分组。在组内,计算每秒的 OrderVol 之和

factor = data.groupby(["Code_Mkt", "Qdate", "Qtime"])["OrderVol"].sum()

# 对比 factor_index,填补缺失值为 0

factor = factor.reindex(self.factors_index_second.index, fill_value=0)

# 按照股票和日期分组。在组内,对于每一秒,计算过去 60 秒的 OrderVol 之和

factor = (

factor.groupby(by=["Code_Mkt", "Qdate"])

.rolling(60, closed="left")

.sum()

.droplevel(level=[0, 1])

)

# 整理格式

factor = self.format_factor(factor)

factor.rename(

columns={

"OrderVol": "A3",

},

inplace=True,

)

factor["A3"] = factor["A3"].astype(float)

return factor

def calculate_A4(self, data: pd.DataFrame = None) -> pd.DataFrame:

"""

Total quantity of arrived orders up to that time

Parameters

----------

data : pd.DataFrame

Order data

Returns

-------

pd.DataFrame

Total quantity of arrived orders up to that time

"""

# 默认使用 self.order,如果指定了 data,则使用 data 中的数据

if data is None:

data = self.order

# 按照股票、日期和秒钟分组。在组内,计算每秒的 OrderVol 之和

factor = data.groupby(["Code_Mkt", "Qdate", "Qtime"])["OrderVol"].sum()

# 对比 factor_index,填补缺失值为 0

factor = factor.reindex(self.factors_index_second.index, fill_value=0)

# 按照股票和日期分组。在组内,对于每一秒,计算当前累积的 OrderVol 之和之和

factor = factor.groupby(by=["Code_Mkt", "Qdate"]).cumsum().shift(1)

# 整理格式

factor = self.format_factor(factor)

factor.rename(

columns={

"OrderVol": "A4",

},

inplace=True,

)

factor["A4"] = factor["A4"].astype(float)

return factor

def calculate_A5(self, data: pd.DataFrame = None) -> pd.DataFrame:

"""

Number of buy orders arriving in the last 60 s

Parameters

----------

data : pd.DataFrame

Order data

Returns

-------

pd.DataFrame

Number of buy orders arriving in the last 60 s

"""

# 默认使用 self.order,如果指定了 data,则使用 data 中的数据

if data is None:

data = self.order

# 筛选出 buy orders

data = data[data["FunctionCode"] == "1"]

# 按照股票、日期和秒钟分组。在组内,计算每秒的 order 数量

factor = data.groupby(["Code_Mkt", "Qdate", "Qtime"])["OrderRecNo"].count()

# 对比 factor_index,填补缺失值为 0

factor = factor.reindex(self.factors_index_second.index, fill_value=0)

# 按照股票和日期分组。在组内,对于每一秒,计算过去 60 秒的 order 数量之和

factor = (

factor.groupby(by=["Code_Mkt", "Qdate"])

.rolling(60, closed="left")

.sum()

.droplevel(level=[0, 1])

)

# 整理格式

factor = self.format_factor(factor)

factor.rename(

columns={

"OrderRecNo": "A5",

},

inplace=True,

)

factor["A5"] = factor["A5"].astype(float)

return factor